Maya Bank reimagines financial autonomy for the next generation

Last week, the Department of Transportation launched a new payment system at the MRT-3: instead of buying a ticket, passengers can simply tap their credit or debit card in select turnstiles.

Despite already being a norm in neighboring countries, this move became a cause of concern for many Filipinos. Many worried that cards could get compromised.

While the jury is still out on this new initiative — and there’s much to be said about the country’s public transport more generally — this response reflects much of our beliefs around money and banking. The majority of us have to jump through extreme hurdles to earn barely enough; it makes sense that anxiety and mistrust define our financial attitudes.

It’s also partly why almost half of the Philippines remain unbanked. Research by McKinsey & Company revealed that brick-and-mortar banks seldom reach rural areas. Relative to banks elsewhere in Asia-Pacific, our banks also allocate fewer resources to developing their digital infrastructure.

Lack of documentation is another barrier, says Angelo Madrid, President of Maya Bank and the Digital Bank Association of the Philippines. “Many Filipinos, especially youth, informal workers, and small entrepreneurs, lack the formal IDs, pay slips, or utility bills that legacy institutions still require,” he tells The Philippine STAR.

“Then there’s the issue of complexity and cost,” Madrid adds. “For decades, banking felt intimidating, with fine print, minimum balances, and hidden fees. For many, it just didn’t feel like it was made for them.”

Filling the gaps of legacy infrastructure

The necessity of e-wallets and online transactions during the COVID-19 pandemic carried over to the new normal, with digital payments now accounting for over 53% of retail sales. It also broke ground for a wider acceptance of digital banks.

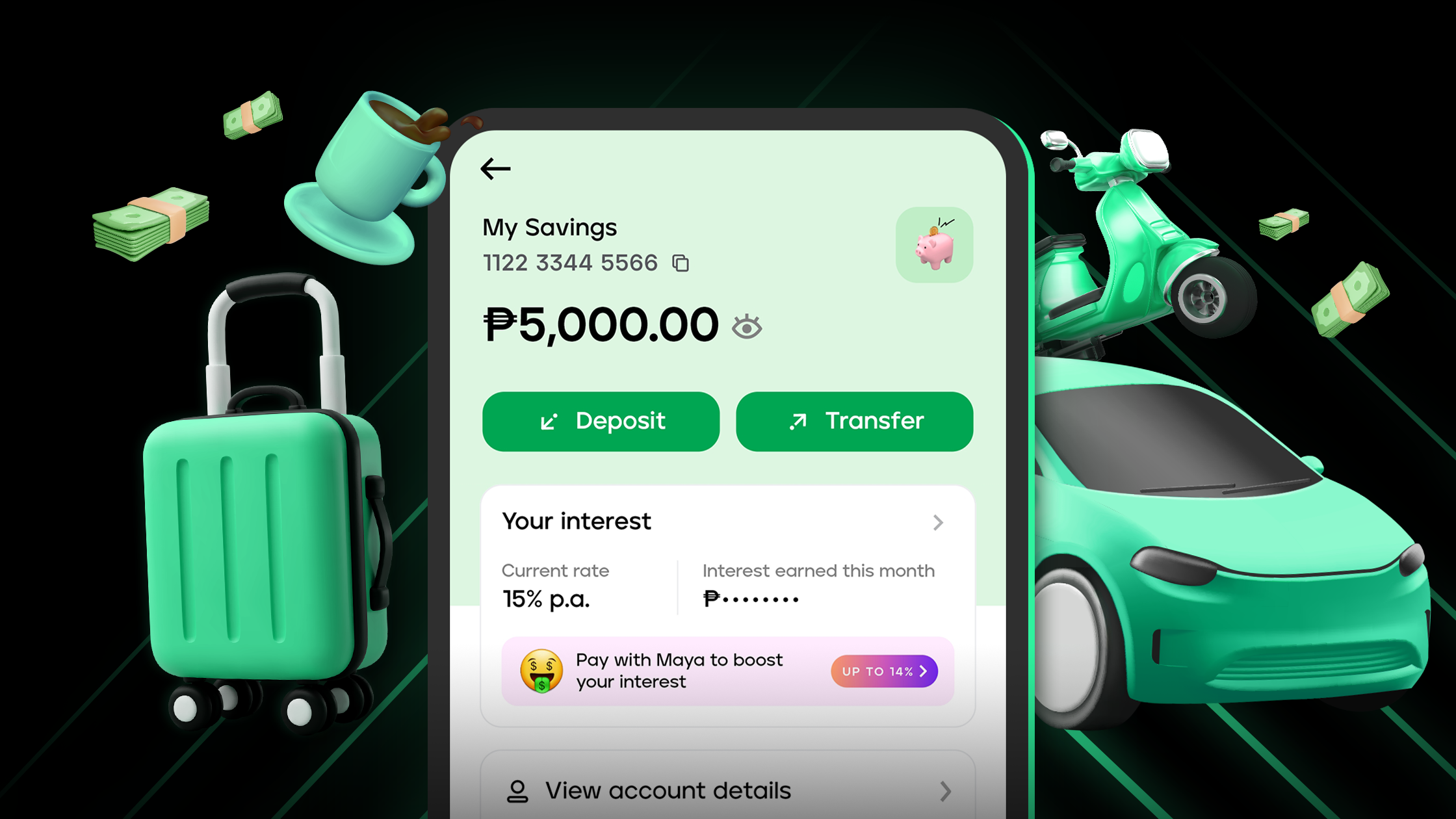

Maya Bank, for instance, has no physical branches, enabling users to complete all transactions through a mobile app. By the end of last year, it reported 5.4 million bank customers.

“We’re making it easier for Filipinos to open an account, build credit, and grow their money anytime, anywhere, through just a mobile phone,” says Madrid. All processes, including loans and credit card applications, are done in-app, without long forms. Beyond convenience, this also expands “access to financial tools that support daily life, long-term goals, and upward mobility.”

While digital-native millennials and Gen Z have been early adopters, Madrid assures that digital banking serves anyone, “from young professionals building their credit for the first time, to small business owners managing cash flow, to retirees looking for better ways to grow their savings.”

“The real power of digital banking is in its flexibility. It adapts to the user, not the other way around.”

But access is just the beginning. “The next step is financial health,” he continues, “helping Filipinos not just open accounts, but actually use them to save, borrow, invest, and grow.”

What does "financial autonomy" mean for a country like the Philippines?

Confidence plays a crucial role in healthier financial habits. Financial autonomy, for Madrid, means “making confident decisions about saving, spending, or building your future.”

Maya Bank’s internal data shows that a growing number of young customers use multiple products in one app: “They use Maya Savings, Personal Goals, and Time Deposit Plus to save intentionally and visualize progress. They rely on Maya Easy Credit, Maya Flexi Loans, and our credit cards for flexible, life-stage support, whether it’s for school expenses, travel, or small business capital.”

Madrid observes, “Young Filipinos aren’t just earning. They want to build discipline, pursue goals, and maintain control of their financial journey.”

While we more commonly associate good money habits with savings, the bank’s accessible credit tools help young Filipinos start creating a credit footprint — something that, Madrid says, “many of them don’t realize they need until much later.” He adds, “Building that history early can open doors: to owning a home, launching a business, or just having access to funds when life gets unpredictable.”

Building trust

Trust is particularly hard to earn as a digital bank, especially with oft-viral horror stories of people getting scammed online. Most Filipinos are also naturally more trusting of the brick-and-mortar bank we have been used to.

Young Filipinos aren’t just earning. They want to build discipline, pursue goals, and maintain control of their financial journey.

Maya Bank uses advanced fraud detection, AI-powered monitoring, and real-time alerts to protect every transaction. It also runs educational campaigns in the app, reminding users how to spot and avoid scams.

That said, Madrid says trust is ultimately earned “by making sure the app simply works.” Constant downtime, apps crashing, and other technical errors are not only inconvenient but also call into question the bank’s reliability and security.

Expanding adoption

Although digital banks can be used by everyone, certain communities may still face barriers, such as poor internet connection and limited digital literacy.

As such, Maya Bank has been rolling out targeted programs for underserved groups. One is Maya Negoserye, an on-ground financial education campaign for MSMEs and sari-sari store owners. It teaches entrepreneurs how to use digital tools, like accepting QR payments and building credit.

FinFit, meanwhile, focuses on promoting financial health among students, teachers, and parents. In partnership with the Department of Education, the program covers saving, managing credit, security, and other digital banking topics.

“These efforts are about meeting people where they are, whether they’re in the classroom, the market, or at home, and giving them the tools to participate,” Madrid says.